U.S. drillers this week added oil rigs for a fourth consecutive week, according to Baker Hughes Inc.’s (NYSE: BHI) closely followed report July 22, with the recent return to the well pad expected to soften the decline in domestic crude production.

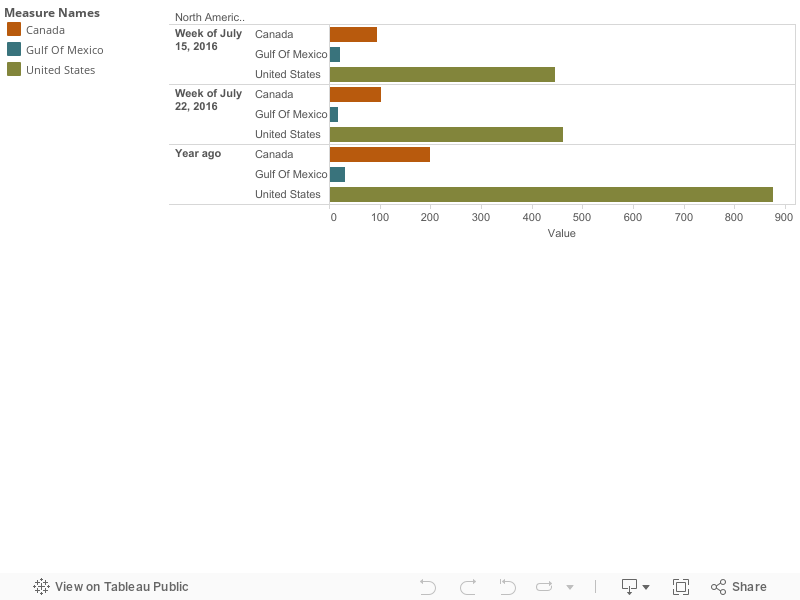

Drillers added 14 oil rigs in the week to July 22, bringing the total U.S. oil rig count up to 371, compared with 659 a year ago, Baker Hughes said. That is the biggest weekly increase since December.

Most of the new rigs were in the Permian Basin in west Texas, where drillers added eight, bringing the total count up to a five-month high of 168.

Other basins with gains this week included the Barnett, D-J/Niobrara, Eagle Ford, Granite Wash and Mississippian. With the exception of the Cana Woodford, where the rig count dropped by one to end the week at 28, other major basins covered in the report had unchanged rig counts.

The total U.S. rig count jumped by 15 to 462; however, the U.S. gas rig count dropped by one to end the week at 88. The number of rigs operating in the Gulf of Mexico also fell and are down by three this week to 18.

Farther north, the Canadian count rose to 102, which is seven more than last week.

In all, the North American count bounced to 564, up 22 from last week, but remained below the 1,076 rigs that were operating about this time last year, according to Baker Hughes.

Since early June when U.S. crude prices settled over $50 a barrel (bbl), U.S. drillers have added 55 oil rigs.

Analysts and producers said $50 was a key level that would prompt a return to the well pad after the steepest tumble in oil prices in a generation prompted a slump in the oil rig count since it peaked at 1,609 in October 2014.

That increased drilling should stop the decline in production in a few months, the U.S. Energy Information Administration (EIA) projected in its latest Short-Term Energy Outlook.

“Higher and more stable crude oil prices are contributing to increased drilling in the United States, which may slow the pace of production declines,” the EIA said.

After sliding every month this year from 9.2 MMbbl/d in January, the EIA expects crude output to bottom at 8.1 MMbbl/d in September before edging up to 8.2 MMbbl/d in October and 8.3 MMbbl/d in November and December. In 2015, production averaged 9.4 MMbbl/d.

“While declines from existing wells are expected to result in a net decrease in production, increased drilling and higher well productivity are expected to soften the decline.”

While U.S. crude futures have dropped back from $50/bbl since late June on renewed oversupply concerns to about $44/bbl on July 22, analysts and companies continue to forecast the rig count will increase during the second half of 2016 and into 2017 and 2018 when prices are expected to rise.

Futures for the balance of the year were trading around $45/bbl, while calendar 2017 was below $49/bbl.

Both Schlumberger Ltd. and Halliburton Co., the world's top two oilfield services providers, said they expect a modest increase in North American activity.

“We believe the North America market has turned,” Halliburton CEO David Lesar said, as the company sees a “modest uptick” in North American rig count in the second half of the year.

Analysts at Simmons & Co. and energy specialists at U.S. investment bank Piper Jaffray, forecast that the total oil and natural rig count would average 487 in 2016, 675 in 2017 and 953 in 2018.

Hart Energy staff contributed to this report.

Recommended Reading

EU Expected to Sue Germany Over Gas Tariff, Sources Say

2024-04-17 - The German tariff is a legacy of the European energy crisis that peaked in 2022 after Moscow slashed gas flows to Europe and an undersea explosion shut down the Nord Stream pipeline.

Pemex to Remain Fiscally Challenged for Mexico’s Next President

2024-04-16 - S&P Global Ratings said Pemex will remain a fiscal challenge for the country’s next president, adding that continued cautious macroeconomic management was key in its ratings on both Mexico and Pemex.

Yellen Expects Further Sanctions on Iran, Oil Exports Possible Target

2024-04-16 - U.S. Treasury Secretary Janet Yellen intends to hit Iran with new sanctions in coming days due to its unprecedented attack on Israel.